There's no doubt the United Kingdom's separation from the EU will have reverberations in the Manhattan housing market, but just what those aftershocks may be is not entirely clear at this early stage.

I’ve already heard from brokers using the Brexit has a negotiating tool and placing low offers on listings, "Hey, I could see you asking that price pre-Brexit, but not post-Brexit!"

As we now know, the markets have recovered and it’s way too early to see exactly what kind of real impact Brexit will have on the Manhattan housing sector. Our super-luxury market is already at a virtual stand still and other price points are near “snookered”!

There are some that say the UK exit might even help the super luxury end of the market as investors from Europe and other overseas markets, which are subjected to even more turmoil and stress, continue to flock to our shores for a much more stable investments. Large cities, such as New York, Miami, Los Angeles and Washington, D.C. could see a nice little bump in their luxury and high-end markets from now to the end of the year.

Long term, though, the general consensus is that the adjustment of removing the U.K. from the EU will be tough on the global economy.

So, what should the average buyer or seller make of all this “barmy” news?

Well, for starters, because of all this unease, the Fed will most likely not raise interests rates to ensure the housing market doesn’t see any more undue stress than it needs to for the remaining part of the year. There may be a further adjustment period to add to our already adjusting marketplace because of the Brexit. Or there could even be a pause in the markets while everyone stops to see what’s going to happen—although this is unlikely in the New York City housing market. Some say this could be beneficial to buyers as sellers might get nervous and accept a lower price then they’d initially take. For sellers, they might feel skittish at the market and feel there is too much uncertainty, removing their properties from the marketplace, depleting the housing stock and putting downward pressure on the buyer's supply causing demand to increase.

But, personally I feel that the market around $1 million will stay strong, maybe even pick up, and that all other segments will carry on the same paths they were headed on before the Brexit vote — at least for the next 6 months.

The Monthly Numbers:

June saw 1,600 new listings come to the market in Manhattan, which is down 869 from May.

In May 23.5% of all new listings that month were in contract by the end of May. Compared to only 17.7% in June.

Across the board June saw a decrees in listings in all categories, which is typical. Listing volume on average 35% and a full 59% in the two-bed category.

2Q16 Manhattan Market Report

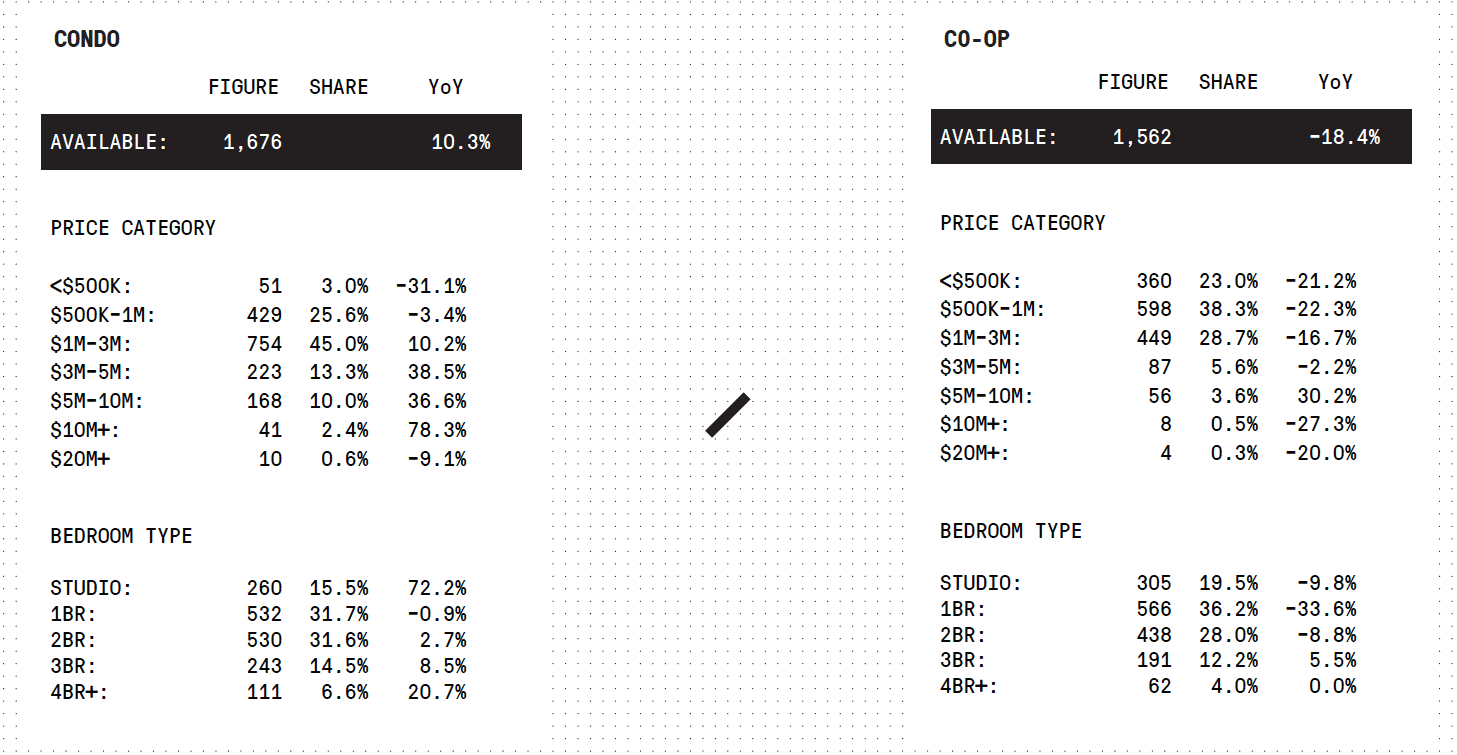

- There were 3,238 closings during the second quarter, a 6% decrease from a year ago. Condo closings increased by 10% while co-op closings decreased by more than 18%, led by a 22% decline in closings under $1M, the property types's largest price segment. Condo sales in both the $3M-$5M and the $5M-$10M categories increased by over 35% compared to last year, largely due to the surge of closings in a number of new developments, most notably The Greenwich Lane, 10 Madison Square West, and 56 Leonard.

- The 2Q16 median closing price was the highest on record for the market overall ($1,195,000), co-op ($795,000), and the highest second quarter on record for condos ($1,650,000).

- Absorption is brisk in the Downtown Market, where median time on market (68 days) nearly matched that of Manhattan overall (63 days) despite a median closing price that was 41% higher than Manhattan's.

- Months of supply is on the rise, as inventory posts slight gains and pace of contract signings slowed.

The Hoffman Team Has Gone Social

Hoffman Team Active Listings

COMPASS News:

- Compass is now one of the top 5 brokerages in both NYC and Washington D.C.

- Compass is home to the top real estate team in the country (The LeonardSteinberg Team) and 14 of the top real estate agents in the county. Dylan Hoffman was #101 out of 2,500,000 agents.